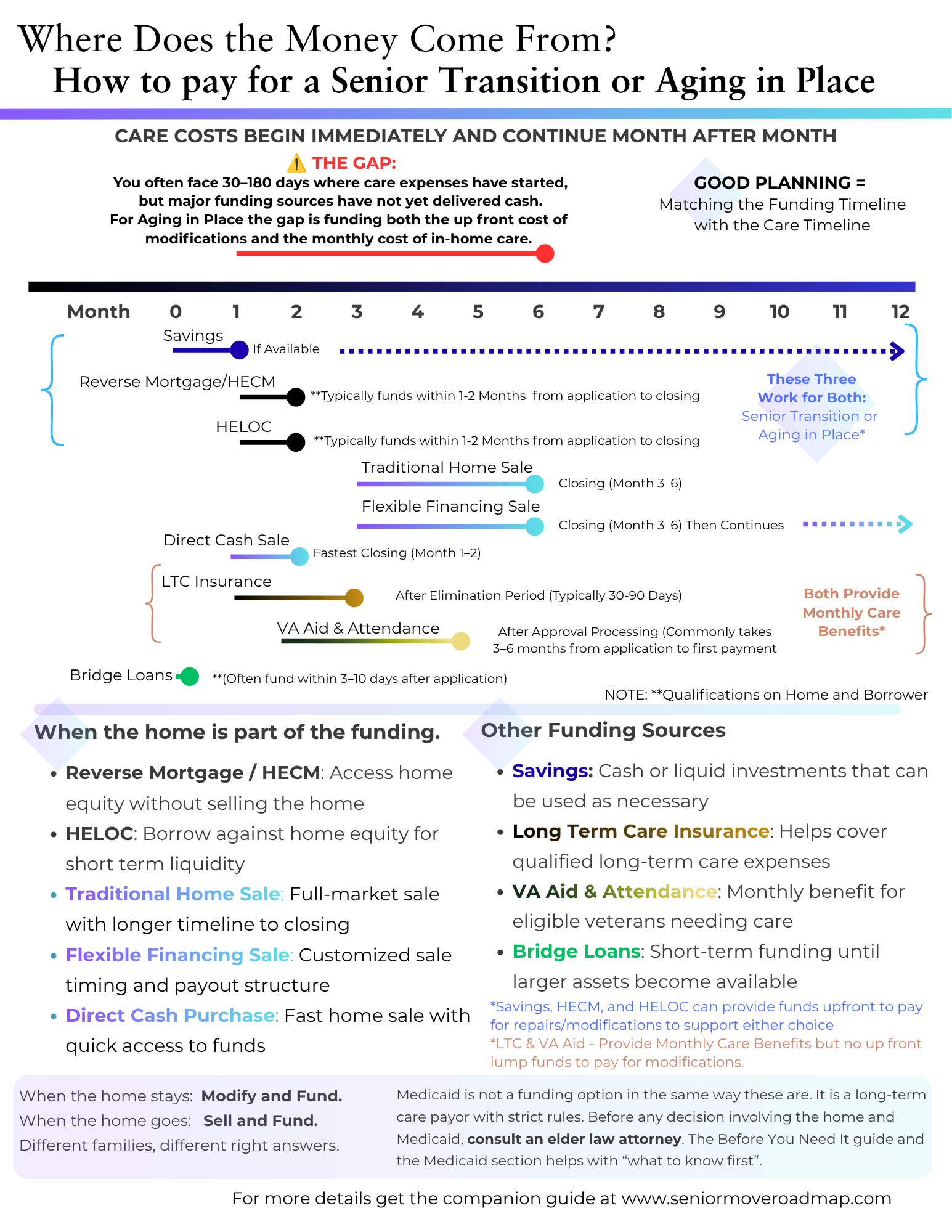

The gap — and why the path matters

Care costs begin immediately. Most major funding sources take 30–180 days. That gap is real, and it works differently depending on your path:

If you’re staying home: The gap is funding both the upfront cost of modifications AND the monthly cost of in-home care. Bucket 1 covers modifications. Bucket 2 covers care. If you assume Bucket 2 covers modifications too, you’ll plan wrong.

If you’re selling: The gap is funding the move and the monthly cost of facility care while the home sells. A traditional sale takes 3–6 months. A direct cash purchase compresses that to 1–2 months. The difference can be tens of thousands of dollars in bridge costs.

The four reverse mortgage questions worth asking

A Home Equity Conversion Mortgage (HECM) is a powerful tool for the stay path. Before signing, ask:

1. Non-borrowing spouse: If your spouse isn’t on the loan, what protections exist if you pass first? The rules changed in 2015 but the protections have conditions.

2. Occupancy: The loan requires the home as primary residence. If you move to a care facility for more than 12 months, the loan may come due. What triggers that, and what’s the process?

3. Taxes and insurance: You still owe property taxes and homeowner’s insurance. Falling behind can trigger default. Is a set-aside account part of your loan structure?

4. Your heirs: When the loan comes due (usually at death or permanent move), your heirs can pay it off or sell the home. They won’t owe more than the home is worth. But they need to know this is coming.

Medicaid is not a funding option in the same way these are. It is a long-term care payor with strict rules. Before any decision involving the home and Medicaid — whether you stay or sell — consult an elder law attorney. The Medicaid protection page walks through the ten questions to bring to that meeting.