The funding timeline, in one picture

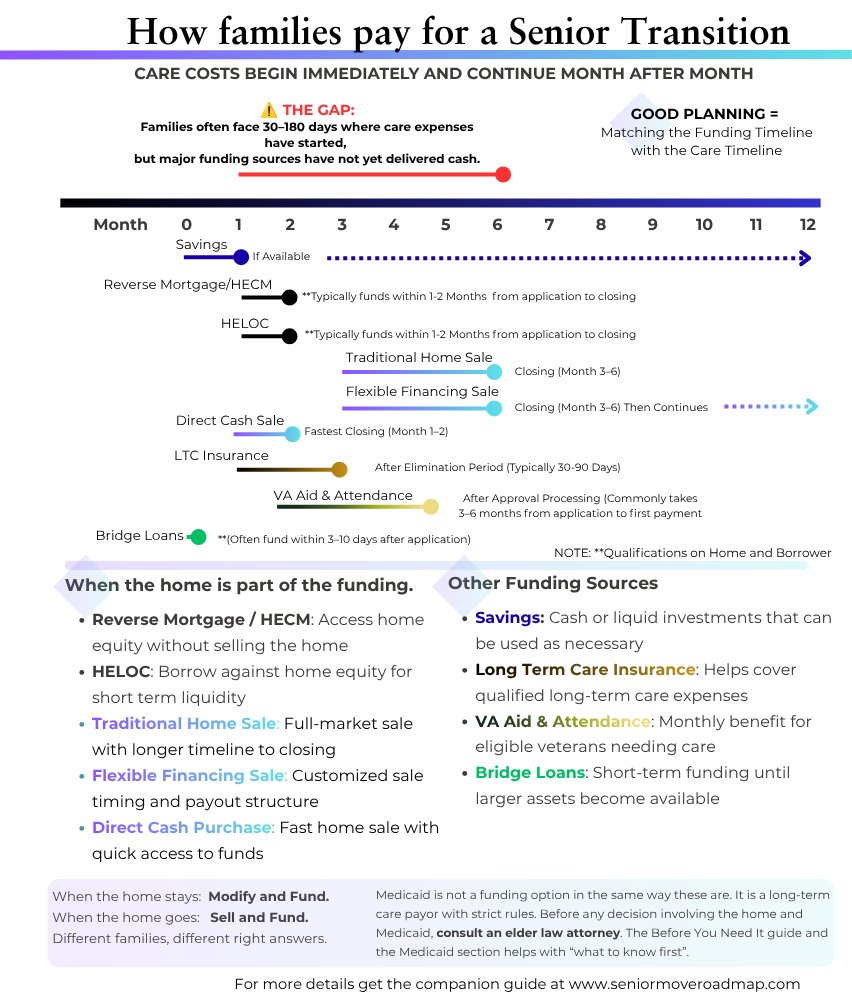

Care costs begin immediately and continue month after month. Funding sources don't. Each one has its own approval timeline — and that gap, between when bills start and when funding lands, is where families get into trouble.

The gap most families miss: Care costs start month 1. Reverse mortgages and HELOCs take 1–2 months to close. A traditional home sale takes 3–6 months. VA Aid & Attendance can take 3–6 months from application to first payment. Without planning, families fund the gap out of savings, retirement accounts, or credit cards — sometimes in the wrong order, with tax and Medicaid consequences they didn't see coming.

The funding sources, one at a time

Below is a working list of every realistic funding source for a senior transition. Each one has a different speed, a different cost, and a different right-fit situation. The map above shows them in time; the sections below explain them in detail.

Reverse Mortgage / HECM

A Home Equity Conversion Mortgage lets a homeowner aged 62+ access home equity without selling. The home stays the borrower's. The loan becomes due when the last borrower permanently leaves the home. Typical timeline from application to closing: 1–2 months. Best fit: a parent who is staying in the home and needs to access equity for care or modifications.

The HECM is powerful and frequently misunderstood. There are four traps families fall into — non-borrowing spouse, occupancy, taxes-and-insurance, and heirs. The Aging in Place guide covers each one honestly.

HELOC (Home Equity Line of Credit)

A line of credit secured by home equity. Faster to close than a HECM (1–2 months) and lower fees, but requires monthly payments and income to qualify. Best fit: a family bridging a known timeline (the home is going to sell in 6 months; the HELOC funds care until proceeds arrive).

Traditional Home Sale

The full-market sale. Highest gross proceeds in most markets, but the longest timeline: typically 3–6 months from listing to closing, sometimes more. Best fit: a family with time, a home in good condition, and no urgent care deadline. Requires the home to be vacant or actively prepared during showings — which is hard when a parent still lives there.

Flexible Financing Sale

A structured sale with custom timing and payout — for example, seller financing, lease-back arrangements, or installment sales. Slower close than a cash sale but more flexible than traditional. Best fit: a family where timing the proceeds matters more than maximizing them.

Direct Cash Purchase

An AS-IS sale to a cash buyer. Closes in 30–60 days. Net proceeds are lower than a traditional sale, but the speed and certainty are real. Best fit: a family in a crisis timeline, or a home in condition that would require significant pre-sale investment.

Savings & Liquid Investments

Available immediately. Worth noting because most families default to spending savings first — which is often the wrong order. Spending tax-advantaged retirement accounts or appreciated investments before home equity can create unnecessary tax bills and reduce the estate. A fee-only financial planner can help sequence the spend.

Long-Term Care Insurance

Helps cover qualified long-term care expenses if the parent has a policy in place. Coverage typically begins after an elimination period (commonly 30–90 days of self-pay). Best fit: a family who is already a policyholder — by the time care is needed, it's generally too late to buy.

VA Aid & Attendance

A monthly benefit for eligible wartime veterans (or their surviving spouses) who need help with daily activities. Worth several thousand dollars per month for those who qualify. Application processing commonly takes 3–6 months from submission to first payment. Best fit: any family with a veteran or veteran's spouse parent — apply early; the back pay is real but the gap can be long.

Bridge Loans

Short-term financing designed to cover the gap until a larger asset closes (typically the home sale). Often fund within 3–10 days of application. Higher rates than a traditional mortgage, but they exist specifically to solve the timing problem. Best fit: a family with a known home-sale plan in motion who needs care funding now.

A note on Medicaid

Medicaid is not a funding option in the same way these are. It is a long-term care payor with strict income, asset, and look-back rules. Before any decision involving the home and Medicaid — gifting, transferring, selling, or restructuring — talk with an elder law attorney. The Before It's Needed Workbook and the Aging in Place guide both reference the rules. Texas families: see also Medicare vs. Medicaid (Texas).

When the home stays, when the home goes

The funding map has two sides. When the home stays (the family chooses aging in place), the funding answer is generally modify and fund — using reverse mortgage, HELOC, or savings to pay for the modifications and care that make staying safe. When the home goes (the family chooses a community move), the answer is generally sell and fund — using the proceeds, sometimes a bridge loan, sometimes flexible sale structures, to pay for the transition and the community.

Different families, different right answers. The map shows both.